If you run a business in Atlanta, Alpharetta, or anywhere else in Georgia, taxes are not a once-a-year event. When income does not have taxes withheld the way a paycheck does, the IRS expects you to pay as you earn, four times a year. Miss those payments and you can get hit with a penalty even if you pay everything you owe by April.

A lot of owners find this out the hard way in their first or second year. The good news is that once you understand how the system works, it becomes routine. This guide walks through who needs to make estimated payments, the 2026 due dates, how much to set aside, and the Georgia rules that sit alongside the federal ones.

Table of Contents

- What quarterly estimated taxes actually are

- Who has to pay them in Georgia

- 2026 estimated tax due dates

- How much to pay and the safe harbor rule

- Georgia estimated taxes, not just federal

- How to actually make the payments

- Common mistakes that cost Georgia owners money

- When it makes sense to bring in a CPA

- Stay ahead of your 2026 payments

- Frequently asked questions

What Quarterly Estimated Taxes Actually Are

Employees have income tax, Social Security, and Medicare taken out of every paycheck. Business owners usually do not. If you are a sole proprietor, a freelancer, a single-member LLC, a partner, or an S corporation shareholder taking distributions, the money you earn often arrives with no tax withheld at all.

Estimated taxes are how you cover that gap during the year. Each quarter you send the IRS a payment that covers your expected income tax plus self-employment tax. Self-employment tax alone runs 15.3% on net earnings, which catches many new owners off guard because it sits on top of regular income tax. You can read the official rules on the IRS estimated tax page.

Who Has to Pay Them in Georgia

The federal threshold is straightforward. If you expect to owe $1,000 or more in tax for the year after subtracting any withholding and credits, you generally need to make estimated payments. For C corporations, the threshold is $500.

In practice, that covers most self-employed people and small business owners in the state. A few examples of who usually needs to pay:

- Sole proprietors and single-member LLCs reporting on Schedule C

- Partners in a partnership and members of a multi-member LLC

- S corporation shareholders whose salary withholding does not cover their full tax

- Landlords and real estate investors with rental income

- Anyone with significant 1099 income, investment income, or side business profit

If your only income is a W-2 salary with enough withheld, you probably do not need to worry about this. But the moment a business or side income enters the picture, the rules apply. Our team often sorts this out during tax planning so owners know their number before the quarter closes, not after.

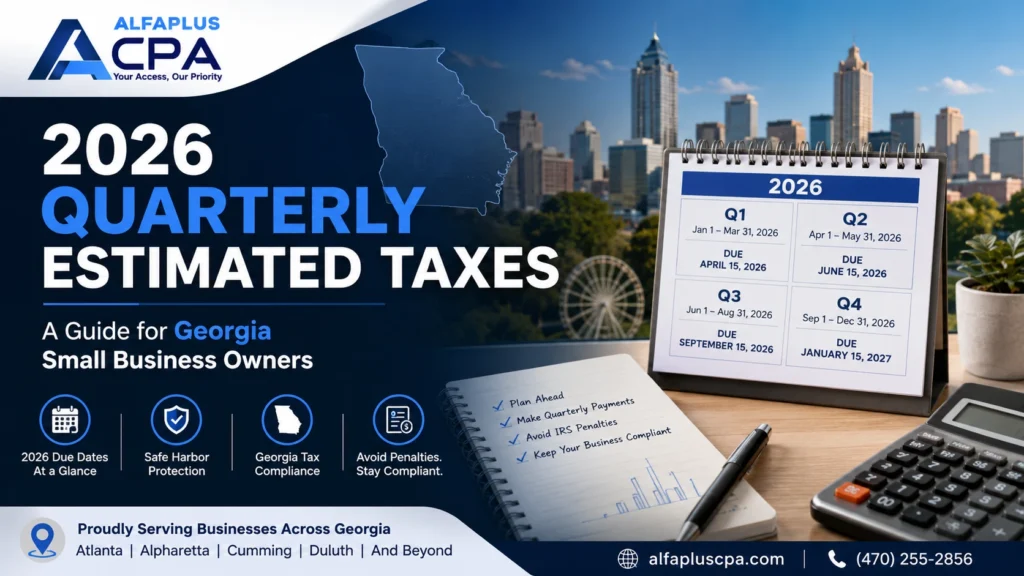

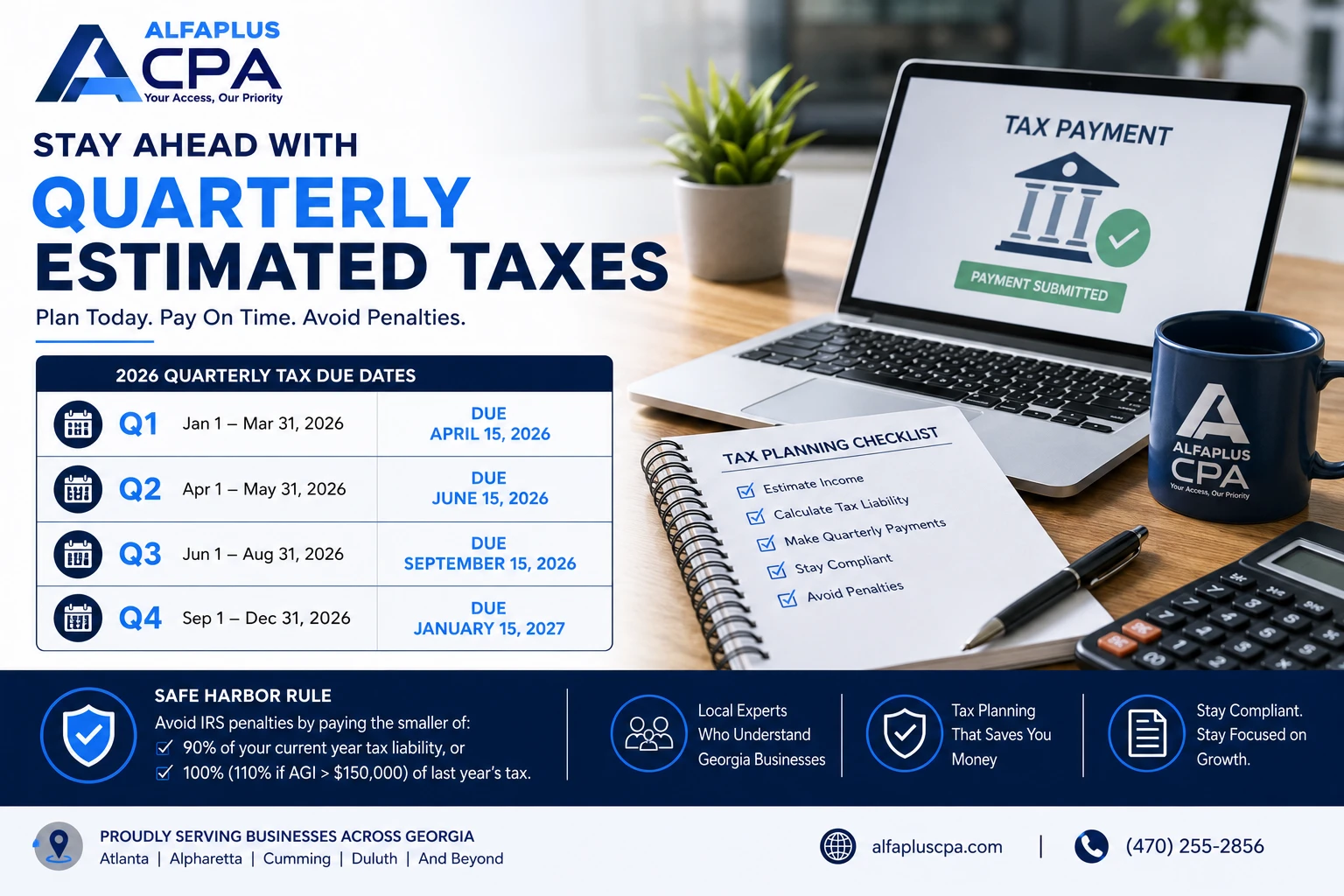

2026 Estimated Tax Due Dates

The federal estimated tax year is split into four payment periods. For the 2026 tax year, the deadlines are:

| Payment Period | Income Earned | Due Date |

|---|---|---|

| Q1 | Jan 1 – Mar 31, 2026 | April 15, 2026 |

| Q2 | Apr 1 – May 31, 2026 | June 15, 2026 |

| Q3 | Jun 1 – Aug 31, 2026 | September 15, 2026 |

| Q4 | Sep 1 – Dec 31, 2026 | January 15, 2027 |

Notice the periods are not even three-month blocks. The second one covers only two months and the fourth covers four. That trips people up, so mark the actual dates rather than assuming they land at the end of each calendar quarter. When a due date falls on a weekend or federal holiday, it moves to the next business day. You can confirm current dates and download the payment vouchers on IRS Form 1040-ES.

How Much to Pay and the Safe Harbor Rule

You do not have to predict your income perfectly. The IRS gives you a safe harbor, which is a level of payment that protects you from the underpayment penalty even if you end up owing more at tax time.

You meet the safe harbor if you pay the smaller of:

- 90% of the tax you will owe for the current year, or

- 100% of the tax shown on last year’s return

There is one catch. If your adjusted gross income last year was more than $150,000, the second number rises to 110% of last year’s tax. For a business that is growing fast, paying based on last year’s smaller tax bill is often the easiest way to stay safe while you figure out where the current year lands.

A simple method many Georgia owners use is to set aside a fixed percentage of every payment they receive—often 25% to 30%—into a separate account. When the quarter ends, the money is already there. If your margins are thin or your income swings a lot, a CPA can build a more precise estimate so you are not overpaying and starving your cash flow.

Georgia Estimated Taxes, Not Just Federal

Federal payments get most of the attention, but Georgia wants its share during the year too. The state has moved to a flat individual income tax, and for 2026 the rate is 4.99% following recent state legislation. Because rates have been changing year to year, it is worth confirming the current figure directly with the Georgia Department of Revenue before you calculate.

Georgia generally expects estimated payments when you have income that is not subject to withholding and you expect to owe more than $500 in state tax. The payment schedule mirrors the federal quarterly dates, and the state uses Form 500-ES for individuals. If you forget the state side and only pay the IRS, you can still face a Georgia penalty. This is one of the most common oversights we see from owners who moved here from a no-income-tax state.

How to Actually Make the Payments

Making the payment is the easy part. Your options include:

- IRS Direct Pay from your bank account, with no fee

- The Electronic Federal Tax Payment System (EFTPS), which is free and lets you schedule payments in advance

- Debit or credit card through an approved processor, which adds a fee

- Mailing a check with the Form 1040-ES voucher

For Georgia, payments go through the Georgia Tax Center online. Keep a record of every confirmation number. If a payment is ever questioned, that record is what clears it up quickly. Good bookkeeping throughout the year makes this painless because your income and expense numbers are always current, not reconstructed in a panic each quarter.

Common Mistakes That Cost Georgia Owners Money

A few patterns show up again and again:

- Forgetting self-employment tax. Owners budget for income tax and get surprised by the extra 15.3%. Plan for both.

- Skipping a quarter after a slow month. The penalty is calculated period by period, so a missed quarter can cost you even if you catch up later.

- Ignoring the state. Paying the IRS but not Georgia leaves a bill and a penalty waiting at filing time.

- Not adjusting after a big change. A strong quarter, a new contract, or selling an asset can push your tax higher. Update your estimates when your income changes.

- Mixing personal and business money. Without a clean separation, calculating what you actually owe becomes guesswork.

If your business is also handling payroll, the timing gets more involved because payroll taxes have their own deposit schedule. Many owners hand that off through payroll services so nothing slips.

When It Makes Sense to Bring In a CPA

You can handle estimated taxes yourself, especially in a stable, simple year. It gets harder when your income is uneven, when you add employees, when you form an S corporation, or when you have income in more than one state. Those are the moments when a small mistake gets expensive.

A CPA does more than calculate a number. They look for deductions and credits you may be missing, keep your federal and Georgia estimates in sync, and adjust the plan as your year unfolds. For business owners, that usually pays for itself. You can see how this fits into a full picture through our business tax preparation service.

Stay Ahead of Your 2026 Payments

Estimated taxes reward owners who plan and punish those who wait. The system is predictable once you know your safe harbor number and the four due dates. Set the money aside, pay on time, and keep both the IRS and Georgia current.

If you would rather not track all of this alone, the team at Alfa Plus CPA works with business owners across Atlanta, Alpharetta, and the rest of Georgia to keep estimated payments accurate and stress low. Schedule a free consultation and we will map out your 2026 payment plan together.

Frequently Asked Questions

Do I have to pay quarterly estimated taxes if my business is brand new?

If you expect to owe $1,000 or more in federal tax for the year, yes, even in your first year. Since a new business has no prior-year return to base the safe harbor on, many owners estimate conservatively for the first few quarters and adjust once they see real numbers. A CPA can help you set a realistic starting figure.

What happens if I miss a quarterly payment?

The IRS charges an underpayment penalty based on how much you underpaid and how long the payment was late. It is calculated for each period, so paying extra in a later quarter does not fully erase a missed earlier one. Georgia can apply its own penalty as well. Paying as soon as you notice limits the damage.

How much should I set aside for estimated taxes in Georgia?

A common starting point is 25% to 30% of your net business income to cover federal income tax, self-employment tax, and Georgia state tax together. The exact figure depends on your total income, deductions, and tax bracket, so treat that range as a safety cushion rather than a precise answer.

Can I just pay everything at the end of the year instead?

You can pay the full balance in April, but if you owed $1,000 or more and did not make quarterly payments, you will likely face an underpayment penalty on top of the tax. The system is built around paying as you earn, so waiting usually costs more.

Do S corporation owners in Georgia need to make estimated payments?

Often yes. S corporation owners take a reasonable salary with withholding, but any additional profit passed through as a distribution usually has no withholding. If that pushes your expected tax over the threshold, estimated payments apply. This is a good reason to review your salary and distribution mix with a CPA each year.