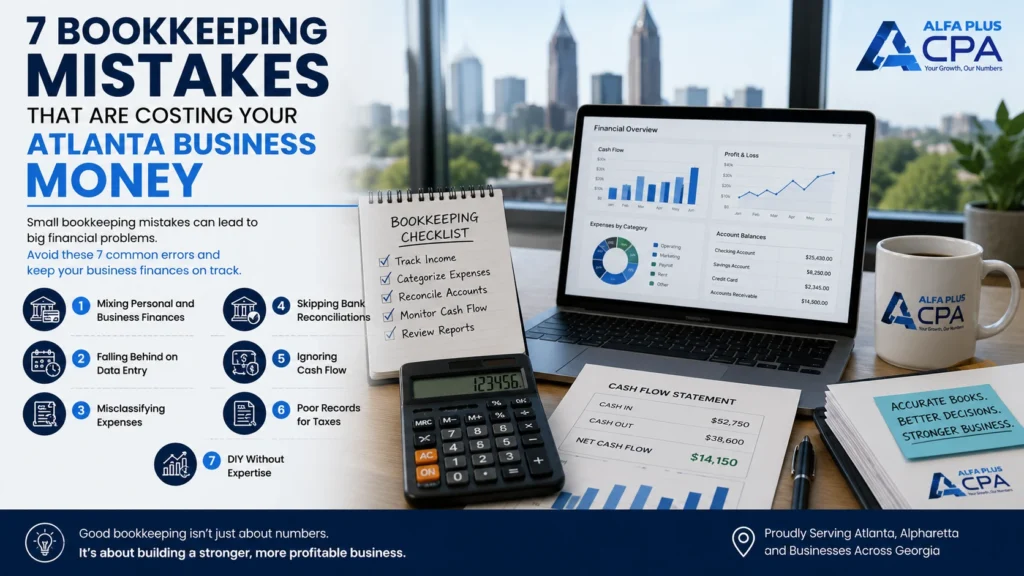

Running a small business in Atlanta is not simple. You’re juggling clients, employees, marketing, operations, and about a hundred other things on any given day. Bookkeeping often gets pushed to the back burner, and that’s understandable.

But here’s the problem: bookkeeping errors don’t just create accounting headaches. They distort your cash flow picture, cost you legitimate tax deductions, raise red flags with the IRS, and lead to decisions based on numbers that don’t reflect what’s actually happening in your business.

The good news is that most bookkeeping mistakes follow predictable patterns. Once you know what to watch for, they’re not hard to correct. Here are seven of the most common ones we see among small business owners in Atlanta, Alpharetta, and across Georgia, along with what to do about each one.

Table of Contents

- Mistake 1: Mixing Personal and Business Finances

- Mistake 2: Falling Behind on Data Entry

- Mistake 3: Misclassifying Expenses

- Mistake 4: Skipping Bank Reconciliations

- Mistake 5: Ignoring Cash Flow

- Mistake 6: Not Tracking Accounts Receivable

- Mistake 7: Trying to Handle Everything Yourself

- What Clean Books Actually Give You

- Frequently Asked Questions

Mistake 1: Mixing Personal and Business Finances

This is the most common bookkeeping mistake, and it’s the hardest to untangle after the fact.

When you pay for a business lunch with your personal card, or cover a personal bill from your business account, you create a mess that affects your financial statements, complicates tax preparation, and can put your personal liability protections at risk if you’re operating as an LLC or corporation.

The fix is simple: open a dedicated business checking account and use a business credit card exclusively for business expenses. Every transaction should have a clear business purpose and a clear paper trail. Once that separation is in place, bookkeeping becomes much cleaner and tax season becomes far less stressful.

If your accounts are already mixed up, our accounting and bookkeeping services can help you sort through the history and get everything properly organized.

Mistake 2: Falling Behind on Data Entry

Some business owners update their books once a quarter, or only when tax season arrives. By that point, you’ve forgotten what certain charges were for, receipts are lost or faded, and categorizing transactions becomes guesswork.

Good bookkeeping should happen on a consistent schedule, either weekly or at minimum monthly. It takes far less time when you stay current than when you let six months pile up into one long, painful catch-up session.

The downstream effects of falling behind go beyond inconvenience. If you can’t see accurate financials in real time, you can’t make good business decisions. You might not notice that expenses in one category have crept up, or that a key client hasn’t paid their invoice in 45 days.

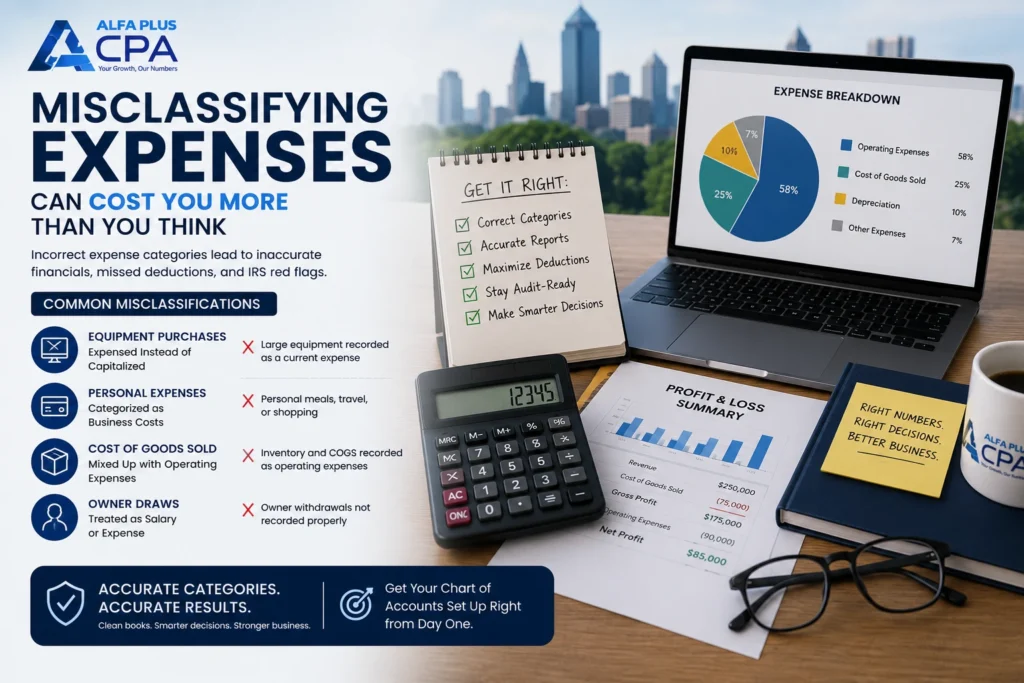

Mistake 3: Misclassifying Expenses

How you categorize expenses matters, both for your financial statements and for your taxes.

If you code a business meal under office supplies, or record equipment as a direct operating expense instead of a capital asset, your reports won’t reflect reality. That can mean overclaiming deductions in one area, underclaiming in another, and financial statements that misrepresent how your business actually operates.

Some of the most common misclassifications include recording equipment purchases as current expenses instead of depreciable assets, categorizing personal expenses as business costs, mixing up cost of goods sold with general operating expenses, and treating owner draws as salary.

These errors are also what IRS auditors look for. If your expense categories don’t line up with standard accounting practices, that can attract scrutiny. The IRS’s own recordkeeping guidelines outline exactly what documentation you need to keep, and how long you need to keep it.

If you’re using QuickBooks or another accounting platform, getting your chart of accounts set up correctly from day one makes a significant difference. Not confident yours is structured right? Our financial consultancy team can review your setup and flag any issues.

Mistake 4: Skipping Bank Reconciliations

A bank reconciliation matches your internal records against your actual bank statements to confirm they agree. It’s one of the most basic internal controls in accounting, and many small business owners skip it because it feels like extra work.

Here’s why it matters: without monthly reconciliation, errors go undetected for months. Duplicate charges, unauthorized transactions, missing deposits, and even fraud can stay hidden in your accounts. When they eventually surface, the cleanup is far more time-consuming than if you’d caught them early.

Reconcile every business bank account and credit card at least once a month. If the balances don’t match, investigate until you find out why. That habit alone prevents a large category of financial problems.

Mistake 5: Ignoring Cash Flow

Your income statement might show a healthy profit, but that doesn’t mean you have cash available to cover payroll next Friday. Profit and cash flow are not the same thing, and confusing them is a costly mistake.

A business can be profitable on paper and still run out of cash if clients pay slowly, inventory is tied up, or large expenses hit at the wrong time. Research from multiple accounting and small business sources consistently identifies cash flow problems as one of the leading reasons small businesses fail. The frustrating part is that the problem is almost always preventable with consistent tracking.

A basic cash flow statement shows when money comes in and when it goes out. You don’t need a complex financial model. You need a clear view of your receivables, payables, and bank balances on a rolling basis so you can see problems coming before they arrive.

Our part-time CFO services are designed for business owners who want that level of financial visibility without adding a full-time finance executive to their payroll.

Mistake 6: Not Tracking Accounts Receivable

You’ve done the work. You sent the invoice. But did you follow up?

Late and unpaid invoices are a cash flow problem hiding in plain sight. Many small business owners don’t have a reliable process for following up on overdue accounts, and some invoices get lost in the shuffle entirely.

Build a habit of reviewing your accounts receivable at least weekly. Know which clients are current and which are past due. Send reminders at 30, 60, and 90 days. If a balance remains unpaid well past 90 days, document it and make a decision about whether to pursue collection or write it off.

Your bookkeeping system should surface this information automatically. If it doesn’t, that’s a setup issue worth fixing. The SBA’s financial management resources also provide practical guidance on accounts receivable practices for small businesses.

Mistake 7: Trying to Handle Everything Yourself

There’s a version of small business ownership where you manage the accounting, payroll, tax filing, and invoicing alongside everything else. Some owners make it work for a while. But time has a cost, and the risk of errors is higher when accounting isn’t your area of expertise.

Hours spent on bookkeeping are hours not spent serving clients, building your team, or growing the business. And small errors compound over time. A misclassified expense or a missed reconciliation in January can create a much bigger problem by December.

Outsourcing bookkeeping, payroll, or tax work to a professional doesn’t mean giving up control. It means getting accurate numbers you can actually trust, with someone in your corner who knows what to look for and can flag problems before they become expensive.

At Alfa Plus CPA, we work with small businesses across Atlanta and Alpharetta at every stage, from startups getting their first set of books organized to established companies cleaning up several years of tangled records. Our HR and payroll services and small business accounting packages are built to be practical and scalable, not complicated.

What Clean Books Actually Give You

Clean, accurate books are not just about compliance or avoiding IRS problems. They tell you whether your business is actually growing or quietly declining, where your money goes each month, and what’s realistic for the next quarter.

When tax season arrives, a business with organized financials pays its CPA for strategy and planning, not for sorting through a year of tangled transactions. That’s a much better use of everyone’s time and money.

If your books are behind, or you’re not confident in what your numbers are telling you, the right time to fix that is now. Not in February when everyone else is scrambling.

Alfa Plus CPA serves business owners across Atlanta, Alpharetta, Roswell, Sandy Springs, and the greater Georgia area. Contact us today for a free consultation, and let’s talk about what your books should be telling you.

Frequently Asked Questions

How often should a small business update its books?

At minimum, monthly. Weekly is better for most active businesses. The more consistently you record transactions, the easier it is to catch errors, track cash flow, and stay prepared for tax deadlines. Businesses with high transaction volume may benefit from daily reconciliation.

What is the difference between bookkeeping and accounting?

Bookkeeping is the process of recording financial transactions on a day-to-day basis. Accounting involves analyzing, interpreting, and reporting on that financial data to support decisions, tax filings, and compliance. A bookkeeper records the numbers; an accountant helps you understand what they mean and what to do about them.

Can poor bookkeeping trigger an IRS audit?

Yes. Certain patterns associated with bookkeeping errors can increase audit risk. Consistently high deductions relative to your income, misclassified expenses, unreported income, or significant inconsistencies between your reported figures and industry norms can all draw attention. Well-organized, accurate records are your best protection if the IRS ever comes knocking. If you’re facing an IRS issue already, our IRS representation services can help.

Do I need accounting software if I hire a bookkeeper?

Most professional bookkeepers use platforms like QuickBooks, Xero, or Wave. Good software makes data entry accurate, reduces manual errors, and gives you real-time access to your own financial information. Even if someone else handles the day-to-day entry, you should always have access to your own accounts and be able to read your own reports.

How do I know if my current bookkeeping setup is actually working?

Ask yourself these questions: How much cash do I have right now? Which clients owe me money and how much? What did I spend in each major expense category last month? Am I profitable? If you can answer all of those questions quickly and confidently from your books, your setup is working. If you can’t, it’s time to review your process.

Alfa Plus CPA provides bookkeeping, accounting, payroll, and tax services to businesses in Atlanta, Alpharetta, and across Georgia. Call us at +1 404-507-2396 or schedule a free consultation to discuss your business’s financial needs.